How to resolve AdBlock issue?

How to resolve AdBlock issue?

News

The trustee of a special needs trust, or SNT, may make discretionary distributions for the “special needs” of a disabled person.

That the trustee has discretion to make distributions and that such distributions are for the beneficiary’s special needs are to preserve the SNT’s beneficiary’s eligibility to receive government needs based benefits, e.g., Supplemental Security Income (“SSI”), Medi-Cal and food stamps.

The government benefits pay only for the beneficiary’s necessities of life (e.g., rent, utilities and food) and the SNT may pay for additional things not covered by such benefits to make a richer life (e.g., vacations, etc.). This way the SNT assets last longer.

When the SNT Trustee provides required accountings to the government caseworker, disagreement can arise over whether the SNT distributions were appropriate under the terms of the SNT and applicable federal and state law. A trustee of an SNT must understand and follow both the SNT’s own distribution standards and the relevant government benefit laws.

In Daniel McGee v. Department of Health Care Services (Super. Ct. No. 12PR7408), the California Third Appellate Court considered what types of distributions for Special Needs a trustee may make from a SNT.

The appellate opinion in McGee addressed whether, “… the term “special needs” … refers only to ‘the beneficiary’s special needs as created by the limitations due to her condition,’ … .”

The court examined the terms of the SNT and applicable federal law and ruled that the term “Special Needs” (i.e., that for which distributions may be made) is not limited only to the beneficiary’s Special Needs created by his or her disability.

Rather the court found that the SNT, “… instrument defines special needs broadly. It declares that the phrase “special needs” broadly means “the requisites for maintaining the Beneficiary’s good health, safety, and welfare when, in the discretion of the Trustee, such requisites are not being provided by any public agency.”

Nonetheless, limitations still exist on what purchases and payments a Trustee of a SNT can make.

The opinion also says that, “the trust instrument did not vest the trustee with sole or absolute discretion to make distributions. Instead, the instrument requires all distributions to be “reasonably necessary in providing for this Beneficiary’s special needs, as defined herein.”

The trustee may make distributions to or for the beneficiary’s benefit in such sums and at such times as the trustee in his discretion determines are “appropriate and reasonably necessary for the Beneficiary’s Special Needs.”

The court also recognized that the SNT instrument allowed the Trustee to make distributions that would reduce or eliminate the beneficiary’s receipt of needs based government benefits if the benefits outweighed the cost.

Thus, for example, the SNT could pay the beneficiary’s rent, and so reduce the beneficiary’s SSI income, if doing so was in the beneficiary’s best interest.

The McGee opinion involved a “First Party” SNT, i.e., an SNT established with the assets belonging to a disabled person, required to meet the federal requirements for a First Party SNT, including that all trust distributions be, “for the sole benefit” of the disabled person, and that, at the disabled beneficiary’s death, the SNT “pay back” to all states the cost of Medi-caid services received in any state.

These other SNT limitations were not relevant to this opinion but play an important part in the drafting and the administration of a “First Party” SNT.

Nonetheless, the discussion in McGee has relevance to Special Needs distributions from all SNT’s, including third party SNT’s, i.e., trusts established by persons other than the disabled beneficiary using assets not belonging to the disabled person.

The foregoing is a brief discussion of how the appellate decision in McGee broadly defined “Special Needs” as it relates to SNT distributions. It is not legal advice. For legal guidance in drafting or administering a special needs trust consult a qualified attorney.

Dennis A. Fordham, attorney, is a State Bar-Certified Specialist in estate planning, probate and trust law. His office is at 870 S. Main St., Lakeport, Calif. He can be reached at

New research from the Stratospheric Observatory for Infrared Astronomy, or SOFIA, has shown that the magnetic fields in 30 Doradus — a region of ionized hydrogen at the heart of the Large Magellanic Cloud — could be the key to its surprising behavior.

Most of the energy in 30 Doradus, also called the Tarantula Nebula, comes from the massive star cluster near its center, R136, which is responsible for multiple, giant, expanding shells of matter.

But in this region near the nebula’s core, within about 25 parsecs of R136, things are a bit weird. The gas pressure here is lower than it should be near R136’s intense stellar radiation, and the area’s mass is smaller than expected for the system to remain stable.

Using SOFIA’s High-resolution Airborne Wideband Camera Plus, or HAWC+, astronomers studied the interplay between magnetic fields and gravity in 30 Doradus. Magnetic fields, it turns out, are the region’s secret ingredient.

The recent study, published in The Astrophysical Journal, found the magnetic fields in this region are simultaneously complex and organized, with vast variations in geometry related to the large-scale expanding structures at play.

But how do these complex-but-organized fields help 30 Doradus survive?

In most of the area, the magnetic fields are incredibly strong. They’re strong enough to resist turbulence, so they can continue to regulate gas motion and hold the cloud’s structure intact. They’re also strong enough to prevent gravity from taking over and collapsing the cloud into stars.

However, the field is weaker in some spots, enabling gas to escape and inflate the giant shells. As the mass in these shells grows, stars can continue to form despite the strong magnetic fields.

Observing the region with other instruments can help astronomers better understand the role of magnetic fields in the evolution of 30 Doradus and other similar nebulae.

SOFIA was a joint project of NASA and the German Space Agency at DLR. DLR provided the telescope, scheduled aircraft maintenance, and other support for the mission. NASA’s Ames Research Center in California’s Silicon Valley managed the SOFIA program, science, and mission operations in cooperation with the Universities Space Research Association, headquartered in Columbia, Maryland, and the German SOFIA Institute at the University of Stuttgart. The aircraft was maintained and operated by NASA’s Armstrong Flight Research Center Building 703, in Palmdale, California. SOFIA achieved full operational capability in 2014 and concluded its final science flight on Sept. 29, 2022.

Anashe Bandari works for NASA.

Lake County News has received reports of community members having thousands of dollars taken from their cards, leaving them unable to pay for rent, groceries and other needs.

Crystal Markytan, director of Lake County Social Services, confirmed to Lake County News that the thefts have been occurring.

“We are able to reimburse victims for loss of their most recent monthly allotment but cannot reimburse over that amount for those recipients who have over one month's allotment stored on their card,” said Markytan.

Markytan added, “This is part of a statewide problem that we have been fortunate enough to largely avoid.”

Rachael Dillman, deputy director over Social Services’ eligibility and employment services, is tracking and reporting the thefts to the state.

Dillman said Lake County residents who are holders of electronic benefits transfer, or EBT, cards are experiencing theft by skimming and scamming.

The Federal Bureau of Investigation reported that skimming occurs when cardholders’ PINs are captured by devices that are illegally installed on ATMs, point-of-sale terminals or fuel pumps.

Criminals then use the data to create fake debit or credit cards and steal from victims’ accounts, the FBI reported.

“It is estimated that skimming costs financial institutions and consumers more than $1 billion each year,” the FBI said on a webpage dedicated to explaining skimming.

Until this month, Dillman said Social Services clients had experienced very little skimming or scamming theft in Lake County, although larger counties throughout the state have been experiencing it for the last few years.

“With each replacement from EBT skimming/scamming theft, we also make a referral to law enforcement for investigation. That does not bar customers from making their own report to law enforcement if they wish to do so,” Dillman said.

She said that from June 1 to 5 alone, there were 49 total cases of skimming/scamming, resulting in $45,325 being stolen. Of that, $41,588 was replaced.

Of those theft cases, Dillman said 37 involved CalWORKs clients, with $34,796 stolen, all of which was replaced.

The remaining 12 clients are in the CalFresh Supplemental Nutrition Assistance Program, or SNAP, program, with $10,529 stolen and $6,792 replaced, Dillman said.

She explained that with CalFresh, Social Services can only replace a maximum of one month's benefits, so if customers were saving up multiple months of benefits, they may have had more stolen than can be replaced under the regulations.

Dillman has been in contact with the California Department of Social Services, and their advice is that customer education is the key to prevention.

As such, Dillman said Social Services has made several postings over the last few months on its Facebook page to educate customers.

In addition, Dillman said the agency has posted notices in its lobbies and handed out informational material to customers when they get their EBT cards.

“I’ve also set a mass emergency text to go out to all customers enrolled to receive text messages reminding them of EBT security and to report theft,” Dillman said.

Safety tips

The Department of Social Services offered the following safety tips to prevent skimming and scamming theft.

If you have an EBT card, follow these tips to keep your benefits safe:

• Keep your PIN and card number secret

• Cover your hand when typing in your PIN

• Change your PIN often, at least once a month the day BEFORE your benefits become available

• Do NOT click on any links from text messages or emails regarding your EBT card

• Watch out for suspicious websites

• Protect your benefits, keep track of your balances daily. There are three ways to check your balance: online at www.ebt.ca.gov or www.benefitscal.com; all 1-877-328-9677, available 24/7; and check your receipt after each purchase.

If you get cash aid, sign up for direct deposit if possible. Bank cards with smart chips are more secure. The state of California is working on updating EBT cards to smart chips, but that won’t begin until 2024.

Check out this video for more safety tips: https://youtu.be/opg52FxKoSo.

Report theft

If you believe your food or cash benefits have been stolen, please call the EBT Customer Services Helpline 24/7 at 1-877-328-9677 or visit your county office right away, Monday through Friday, 8 a.m. to 5 p.m., telephone 707-995-4200, TTY 711, 15975 Anderson Ranch Parkway, Lower Lake.

You may be eligible to have the stolen benefits replaced by completing the EBT 2259 form. You may also wish to file a police report, but that is not required to have your benefits replaced, the Social Services Department reported.

Email Elizabeth Larson at

The hitch is the focus of an emergency declaration the Board of Supervisors passed in February.

The Governor’s Office reported that it has dedicated $71 million to address drinking water shortages, species protection and populations particularly impacted by drought.

Those projects include $500,000 to fund stream gages and well transducers for use in Clear Lake to better understand the relationship between streamflow, well pumping and water use.

The second project, for a contract to investigate groundwater/stream water interactions in the Clear Lake region, also will receive $500,000 for a contract to investigate groundwater/stream water interactions in the Clear Lake region.

The funding for both, totaling $1 million, will support the threatened Clear Lake hitch.

Other awards that are part of that funding round include:

• $10 million to provide immediate and near-term financial and technical support to help small communities whose water supplies have been impacted by drought.

• $55 million to address dry wells by providing hauled water and well repair and replacement.

• $5 million to provide direct relief grants for small-scale and historically underserved farmers.

CLEARLAKE, Calif. — Clearlake Animal Control has several additional dogs ready to be adopted out to new homes this week.

The shelter this week has 43 adoptable dogs.

This week’s adoptable dogs include three Alaskan husky mixes — “Bippity,” “Boppity” and “Boo.”

Bippity and Boppity are both females, Boo is a male.

Bippity has a tricolor coat, Boppity’s coat is black and tan and Boo is black and white.

The shelter is located at 6820 Old Highway 53. It’s open from 9 a.m. to 6 p.m. Tuesday through Saturday.

For more information, call the shelter at 707-762-6227, email

This week’s adoptable dogs are featured below.

Email Elizabeth Larson at

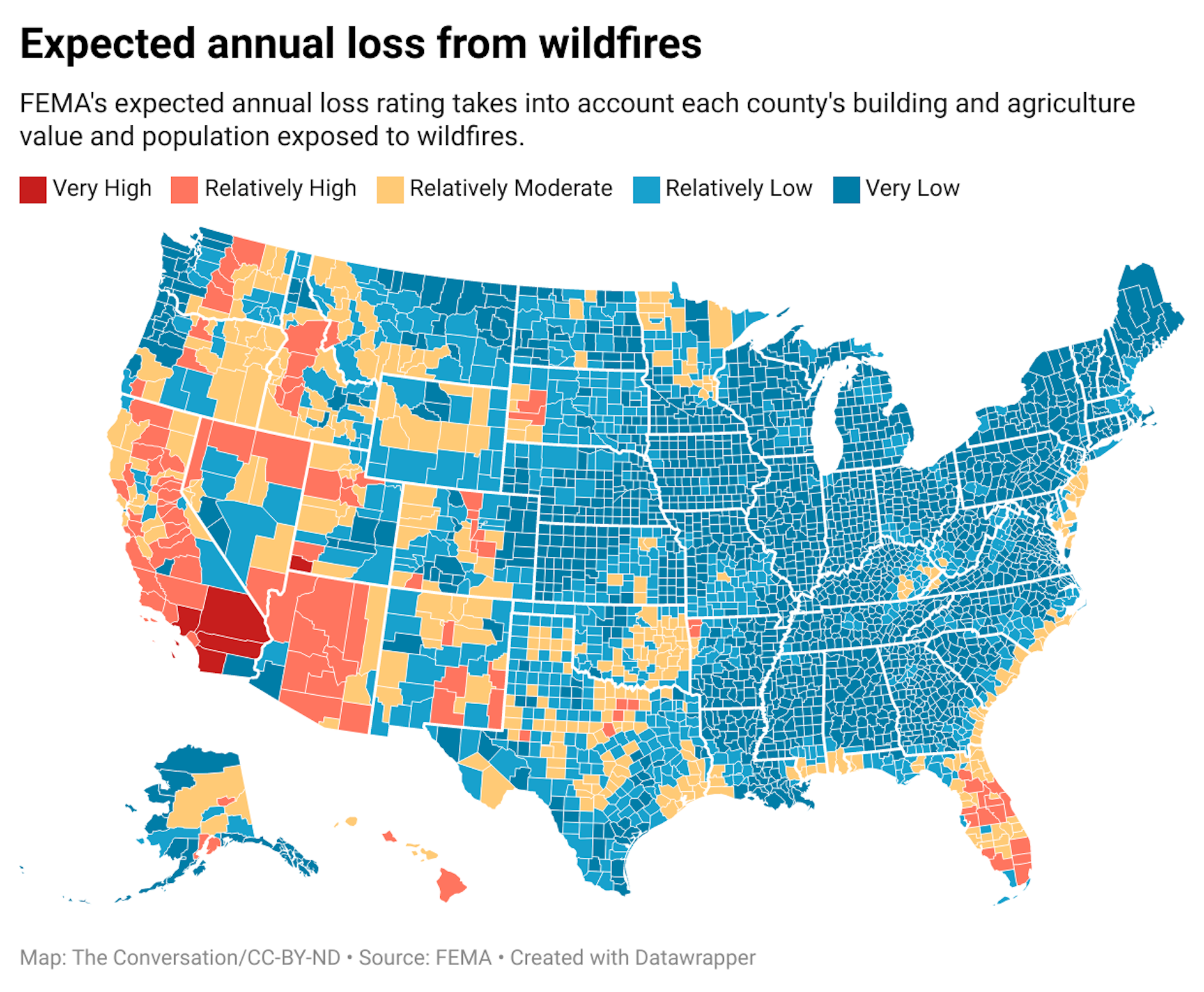

When the nation’s No. 1 and No. 4 property and casualty insurance companies – State Farm and Allstate – confirmed that they would stop issuing new home insurance policies in California, it may have been a shock but shouldn’t have been a surprise. It’s a trend Florida and other hurricane- and flood-prone states know well.

Insurers have been retreating from high-risk, high-loss markets for years after catastrophic events. Hurricane Andrew’s unprecedented US$16 billion in insured losses across Florida in 1992 set off alarm bells. Multibillion-dollar disasters since then have left several insurers insolvent and pushed many others to reevaluate what they’re willing to insure.

I co-direct the Center for Emergency Management and Homeland Security at Arizona State University, where I study disaster losses and manage the Spatial Hazard Events and Losses database (SHELDUS). As losses from natural hazards steadily increase, research shows it’s not a question of if insurance will become unavailable or unaffordable in high-risk areas – it’s a question of when.

Reinsurers are worried

Insurance is a vehicle to transfer risk. When an individual buys an insurance policy, that person pays to transfer the risk of expensive repairs to the insurer if the home is damaged by a covered event, like a fire or thunderstorm. Most policyholders don’t experience major disasters, so insurance companies make money.

However, disasters are extremely costly when they do occur, so insurers also buy their own insurance, called reinsurance.

Reinsurance costs have been rising fast in response to expensive disasters around the world in recent years. Reinsurers’ risk-adjusted property-catastrophe prices rose 33% on average at their June 1, 2023, renewal, after a 25% rise in 2022, according to reinsurance broker Howden Tiger’s analysis.

If prices are too high and insurers can no longer transfer excessive risk to the reinsurance market, they are stuck “holding the risk” – meaning the cost of claims when disasters strike. A big enough disaster can put insurance companies out of business, or they can decide to leave the state, as seen in California, Louisiana and elsewhere.

Responsible insurers are not in the business of gambling, so they do what State Farm and Allstate did: They reevaluate their portfolios – the various lines of insurance they offer, such as auto, life, property insurance and health insurance – and their prices. Insurance is a highly data-driven business and uses some of the most sophisticated climate and risk modeling in the world to forecast future risks, including the likelihood a property will be damaged by wildfire or other natural hazards.

State Farm cited “catastrophe exposure” as a reason for ending new high-risk personal and commercial property and casualty policies in California. That refers to the likelihood that costly claims would exceed the risk State Farm was willing to accept.

{kind=link}

Why drop only California?

So, why did State Farm and Allstate only stop new policies in California and not in other wildfire-prone states like Colorado or Arizona?

The answer can only be speculative since State Farm or Allstate don’t publicly disclose their exposure. That’s calculated based on how many personal and commercial property and casualty policies the company holds in the state, particularly in the wildland-urban interface where fire risk is higher, and at what value.

State Farm did cite California’s increasing wildfire risk and home construction prices, but there are other influences to consider.

One is state insurance regulations that can limit premium increases, prohibit policy cancellations and require certain levels of coverage. Insurer Chubb’s chief executive mentioned restrictions that left it unable to charge “an adequate price for the risk” as part of the reason for its 2022 decision to not renew policies for expensive homes in high-risk areas of California. California also has a unique “efficient proximate cause” rule that forces property insurers to also cover post-fire flooding, such as mudslides. Rainy winters like 2023’s often trigger destructive mudslides in wildfire burn areas.

What happens now?

When insurers pull out of a community, residents and companies without access to property and casualty insurance are left holding their own risk – and paying the price if a disaster strikes. From a societal and political perspective, that’s a problem.

Residents and businesses without insurance tend to recover more slowly. Uninsured residents often depend on donations, loans or federal individual assistance. The latter, however, is only available for catastrophic disasters and covers only immediate needs.

To fill the gap and provide access to insurance, states including California, Florida, Louisiana and Texas have created either private or public insurance options of last resort with generally very pricey premiums.

Residents covered by these options transfer their risk to the state, such as in Louisiana and Florida – meaning state taxpayers, who fund the state insurance programs, hold the risk directly or indirectly. In California, the privately insured FAIR Plan, in existence since 1968, wrote close to 270,000 policies in 2021, nearly double the number in 2018.

Similarly, anyone purchasing flood insurance through the National Flood Insurance Program since 1968 is transferring their risk to federal taxpayers. The NFIP currently insures almost $1.3 trillion in value across 5 million policies.

Politicians are not catastrophe risk experts, though, and do not make decisions based on data alone.

In the short term, I expect that insurance pools, as well as federal- and state-run insurers of last resort, will add more policies, and that state legislators will incentivize the return of insurers. But while the political willingness to support such a trend exists, the financial resources do not.

The National Flood Insurance Program has plenty of lessons to teach about the challenges of balancing exposure and keeping premiums affordable: It is more than $20 billion in debt. Texas has resorted to charging insurers operating in the state to help cover its program’s costs.

Fixing insurance starts with the property itself

Despite the risk of properties becoming uninsurable, communities today continue to permit development in floodplains, along coastlines and in the wildfire-prone wildland urban interface. Inadequate building codes allow developers to build homes that cannot withstand severe weather. These practices have placed millions of residents and the things they value in harm’s way.

As climate change continues to dial up the frequency and severity of natural hazards, there are some steps states and communities can take involving property to lower the risk:

-

Make smarter land use choices and limit development in high-risk areas to avoid placing people and the things they value in harm’s way.

-

Adopt more stringent building codes and safety standards at state and community levels.

-

Price risk into home sales, either through an insurance contingency that allows the buyer to withdraw when they cannot secure insurance or lower assessed property values for real estate in high-risk areas, which can dissuade builders and buyers.

-

Require comprehensive disclosures of all present and future risks along with historic claims associated with a property to educate potential buyers.

-

Make risk information accessible and understandable. My research shows that most people have a hard time fully grasping how likely they are to be affected by a catastrophic event. They need better tools that communicate the information in a way that resonates with them.

-

Help residents in high-risk areas relocate through buyouts and managed retreat that returns the land to nature or public uses such as parks.

Melanie Gall, Assistant Professor and Co-Director, Center for Emergency Management and Homeland Security, Watts College, Arizona State University

This article is republished from The Conversation under a Creative Commons license. Read the original article.